M&A : Investment Trends in Aerospace and Defence

Given the current state of the global economy, investors are becoming increasingly cautious and risk averse about their portfolio investments. This translates into a restraint for the aerospace and defence (A&D) industry as it is capital intensive and investors are unwilling to commit sizeable amounts of money to an industry that has a longer gestation period compared to other industries. However, there may be potential opportunities for investors who are looking for secondary buyouts owing to lower valuation multiples.

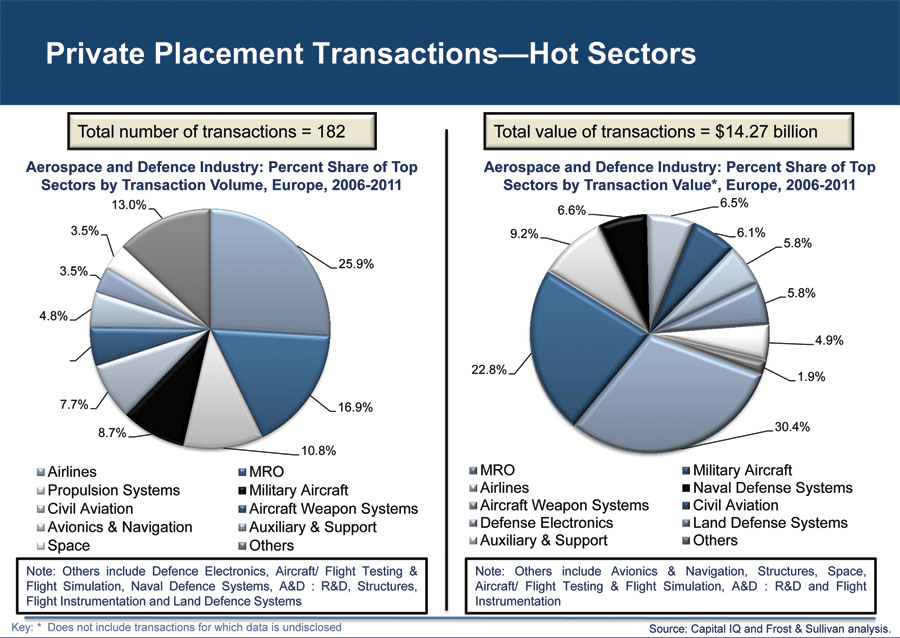

A new analysis from Frost & Sullivan on Equity and Venture Capital Investment Trends in the Aerospace & Defence Industry in Europe, finds that the value of private placement transactions in the European aerospace and defence industry has decreased from $7.05 billion in 2009 to $3.77 billion in 2011. In the same time frame, the percentage of value of private placement transactions in the aerospace and defence industry compared to private placements across all industries has decreased from 2.88 per cent to 1.84 per cent in Europe.

Between 2006 and 2011, around 65 per cent of private placement transactions in the European A&D industry were in the $1 million to $100 million range suggesting that investors have predominantly stuck to lower value deals. Sectors that have attracted investments include A&D maintenance and services, military aircraft, airlines and naval defence systems among others. The first two alone account for over 50 per cent of transactions by value.

Some of the key factors that are expected to drive growth in the industry include aircraft replacement needs faced by mature markets, and growth in emerging markets.

Airbus expects the global passenger fleet to more than double from the existing 15,000 to nearly 31,500 aircrafts by 2030. This is likely to include around 27,800 new deliveries of which 10,500 will be needed for replacing old aircrafts.

"The increasing percentage of the middle class population, especially in countries such as India, China, and Russia, is expected to create demand for the purchase of over 3,500 planes (which is roughly 15 per cent of the global demand) over the next two decades," notes Frost & Sullivan Financial Analyst, Mr. Bharath M.

India and China are among the preferred countries for investments because of lower costs compared to their Western counterparts. By 2030, Asia-Pacific is expected to account for a 33 per cent share of passenger traffic, followed by Europe at 23 per cent and North America at 20 per cent. "Routes connecting these markets are expect to drive investments into the hubs in Middle East and Turkey with investment opportunities in ATM, MRO and especially in the Civil Security sector. New airports will increasingly be a driver of growth and create a new category of cities, Smart Airport Cities, build around the air-traffic hub", notes Managing Director of Frost & Sullivan Turkey, Mr. Philipp Reuter.

Additionally, "due to these growing centers, many original equipment manufacturer (OEM) integrators such as Airbus and Boeing as well as suppliers as GE and Rolls Royce are shifting their production facilities and investments to these strategic location", remarks Philipp Reuter. "A further driver for investments in location were technology excellence is available is the trend to reduce manufacturing costs by outsourcing more ‘design-to- build’ packages rather than just ‘build-to-print’ to Tier 1. Already today we can observe how countries like Turkey and Russia are starting to benefit from this shift."

In a medium term this developments will ultimately have a positive effect also on the mature markets and will vitalize the investment activities in Europe and the US, turning established medium sized companies into interesting targets for investments or for M&A activities by growing players of the (so called) emerging world.

In other words the existing supplier network of the OEMs will not only move to new regions due to the slowdown in Europe, the US and other above mentioned reasons, but in medium term technology advancements of local suppliers will attract capital and drive a new expansion strategy into mature markets.

North American and major Western European economies (currently affected by the Eurozone crisis) are going now in for austerity measures. Defence spending is likely to be reduced in the next two years and this is expected to subdue activity in the industry. We may see valuations of companies going down. While short-term investors will try to exit (by selling a part of their stake), an opportunity exists for long-term investors as a result of low valuations. Companies that have a significant cash-to-assets ratio have an opportunity to grow inorganically.

The key sectors that attracted investments during the 2006–2011 period include MRO, airlines and Military Aircraft. Sectors such as Aerospace Transportation Support Systems and Flight Communications Related Systems are expected to attract investments in the coming months are there is a need for better communication systems that help air traffic control to coordinate with flights and thereby improve the effective aircraft utilization rates.

Out of the 182 transactions analyzed in the study period (January 2006 to December 2011), 83 are from Russia. This is close to 46 percent of all transactions analyzed. The total value of these transactions is around $7.89 billion. This is almost 55 percent of the total value of transactions in Europe in the study period. Some of the drivers of this include vast territory, replacement need of old equipment, rising status of citizens, and Russian manufacturers‘ growing demand for high-quality parts and components. However, opportunities for investors is very limited as strict laws and regulations govern foreign investments. Even local investors face uphill challenges in the industry because it is heavily monitored by the state. For strategic investors, opportunities exist in the form of alliances and joint ventures. Compared to setting up subsidiaries (which can prove to be difficult), Western European companies also have the option of sharing intellectual property rights (such as patents or technical know-how) with their Russian counterparts.

Leasing market is gaining momentum as companies are finding it increasingly difficult to raise capital to purchase new equipment. Also, leasing offers flexibility of operations and is an off-balance sheet liability. Opportunities exist for companies that offer services such as MRO, for lessors.